You’ve tried budgeting before. You tracked expenses for two weeks, felt guilty about the takeout, and quietly abandoned the spreadsheet by the 20th. The problem wasn’t you — it was that your budget described your money instead of directing it. This guide teaches you zero-based budgeting: the method that assigns a job to every single dollar before the month begins, and exactly how to run it without giving up on day 12.

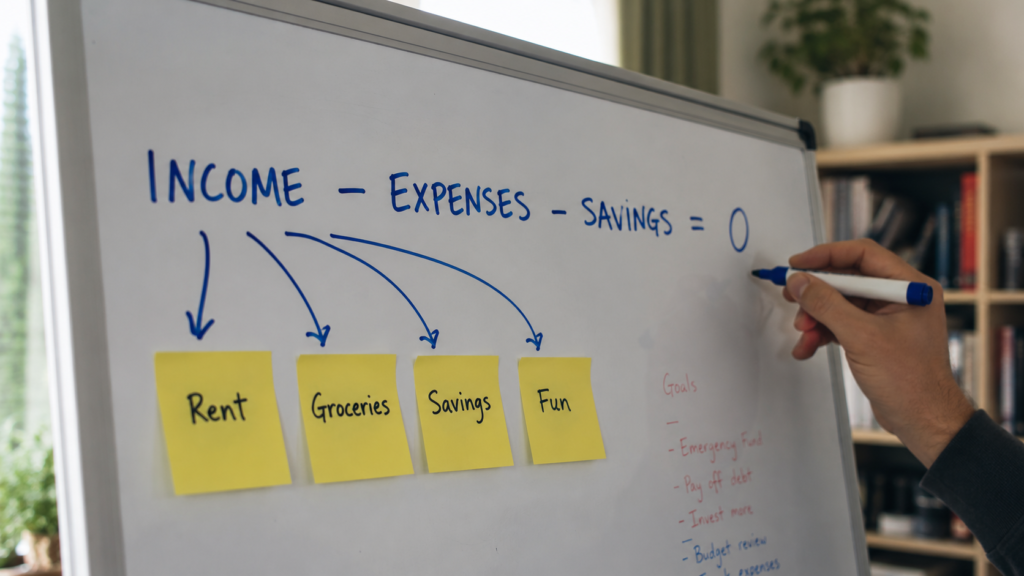

Zero-based budgeting is a method where your income minus your planned expenses equals exactly zero. Before the month starts, you assign every dollar you earn to a specific job — rent, groceries, savings, debt, even fun money — until nothing is left unassigned. It doesn’t mean spending everything; money sent to savings counts as “spent” on savings. The goal is simple: no dollar sits around waiting to be wasted.

Key Takeaways

- Zero-based budgeting means income minus assigned dollars equals zero — every dollar gets a specific job, including dollars assigned to savings and fun.

- You budget before the month starts, using last month’s income if your pay is irregular, so you’re directing money instead of reviewing damage.

- A “budget zero” is not a “bank account zero” — your account should still hold a buffer of at least one month of essential expenses over time.

- When a category runs dry mid-month, you move money between categories instead of quitting; adjusting is the method working, not failing.

- Expect the first two months to feel messy. Most people underestimate 3–5 categories the first time, and that’s normal calibration, not failure.

- You need one honest hour to set it up and about 15 minutes a week to maintain it.

What Zero-Based Budgeting Actually Means (And What It Doesn’t)

Zero-based budgeting is a planning method where you allocate 100% of your income to named categories before you spend a single dirham, dollar, or euro of it. The formula is blunt: income − expenses − savings − debt payments = 0.

Here’s the part beginners get wrong on day one: the zero refers to unassigned money, not to your bank balance. If you earn $3,200 a month, you create a plan where all $3,200 has a destination. Maybe $1,400 goes to rent, $450 to groceries, $300 to a car payment, $250 to savings, $150 to a sinking fund for car repairs, and so on — until the “left to assign” number reads exactly zero. Your checking account can (and should) still hold money. The plan is what hits zero.

The method has a longer pedigree than most people realize. It started as a corporate accounting practice in the 1970s, developed by Peter Pyhrr at Texas Instruments, where departments had to justify every expense from scratch each cycle instead of copying last year’s numbers. Personal finance borrowed the core idea: nothing gets funded by default. Your gym membership, your streaming subscriptions, your Friday takeout — each one has to earn its spot every single month. You can read a deeper technical breakdown of the corporate origins on <a href=”https://www.investopedia.com/terms/z/zbb.asp” target=”_blank” rel=”noopener”>Investopedia’s zero-based budgeting page</a>.

Why does this beat ordinary expense tracking? Because tracking is backward-looking. You find out in week three that you spent $280 on food delivery, feel bad, and change nothing. Zero-based budgeting is forward-looking: the decision about that $280 happens before the month starts, when you’re calm and rational, not at 9 p.m. on a Tuesday when you’re hungry and tired. You’re negotiating with your future self while your future self isn’t in the room. That’s the entire psychological trick, and it’s why the method works when others don’t.

One honest caveat: this is the most hands-on budgeting method there is. If you want something you set once and forget, this isn’t it. What you get in exchange for the effort is total visibility — you will know, at any moment, exactly what every dollar you own is supposed to be doing.

How to Build Your First Zero-Based Budget in 5 Steps

Setting up your first zero-based budget takes about an hour, and the sequence matters more than beginners think. Do these steps in order.

Step 1: Establish your real monthly income. Not your salary on paper — the number that actually lands in your account after taxes and deductions. If you’re salaried, this is easy. If your income is irregular (freelance, commission, tips), use the lowest monthly income from your last six months as your planning number. Budgeting off your best month is how irregular earners blow up their plan. Anything you earn above the baseline gets assigned when it arrives, not before.

Step 2: List your fixed obligations first. Rent or mortgage, utilities, insurance, minimum debt payments, phone, internet. These are non-negotiable in the short term, so they claim their dollars first. For most households, this eats 50–65% of income immediately. Seeing that number in writing is uncomfortable and useful in equal measure.

Step 3: Fund your true monthly variables with real numbers. Groceries, fuel, household supplies. Here’s the calibration trick: open your bank statement from last month and add up what you actually spent on groceries. Don’t budget the aspirational $300 when your history says $520. A budget built on wishes fails by week two. Budget $520 now; shrink it by $30–40 a month once the system is running.

Step 4: Assign dollars to irregular expenses — this is the step that separates people who stick with it from people who quit. Car repairs, annual insurance premiums, holiday gifts, back-to-school costs. These aren’t emergencies; they’re predictable expenses with unpredictable timing. Divide the annual cost by 12 and fund that amount monthly into what’s called a sinking fund — a category where money accumulates for a known future expense. If car maintenance runs you roughly $600 a year, that’s $50 a month, every month, whether the car breaks or not. When the repair comes, the money is already there and your budget doesn’t even flinch.

Step 5: Assign every remaining dollar until you hit zero. Savings goals, extra debt payments, and — do not skip this — a fun money category with your name on it. A budget with no pleasure line item is a crash diet, and crash diets end in binges. Even $40 of truly guilt-free money changes how the whole month feels. When “left to assign” shows zero, you’re done. The U.S. Consumer Financial Protection Bureau offers a free <a href=”https://www.consumerfinance.gov/consumer-tools/budgeting/” target=”_blank” rel=”noopener”>set of budgeting worksheets</a> if you want a structured starting template.

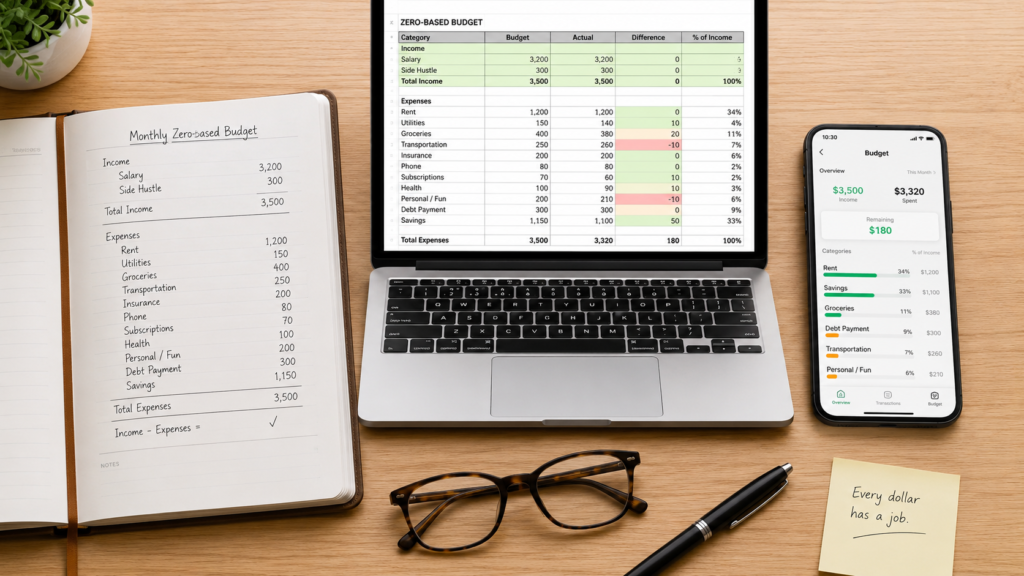

A worked example on a $3,200 net income: housing $1,400, utilities and phone $210, groceries $520, transport $260, insurance $140, debt minimums $200, sinking funds $180, savings $200, fun money $60, giving $30 — total $3,200, left to assign: $0. Every dollar employed.

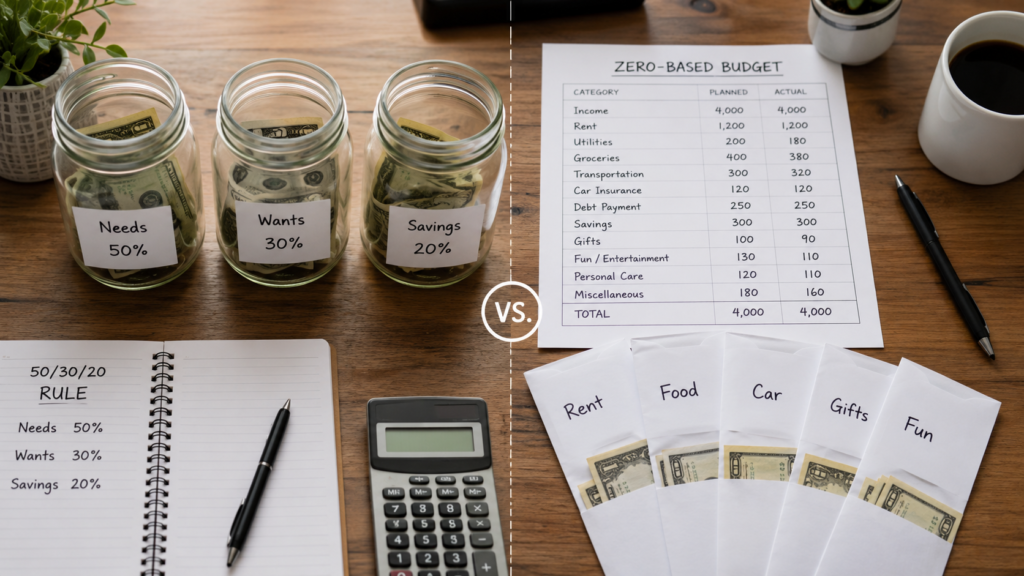

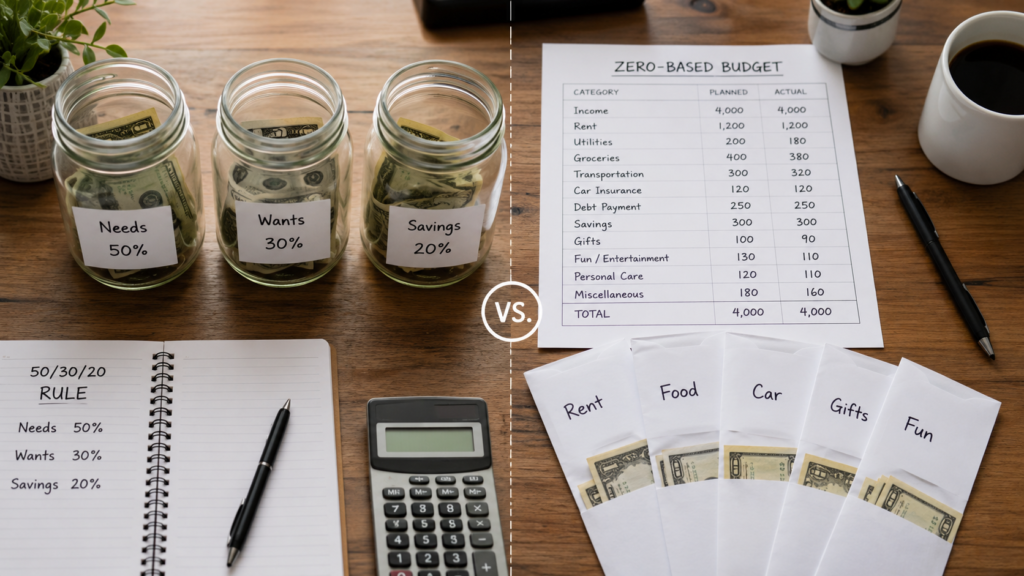

Zero-Based Budgeting vs. the 50/30/20 Rule and Pay-Yourself-First

Choosing between zero-based budgeting and the other popular methods comes down to one question: how much control do you need right now? Here’s how the three most common approaches compare.

| Zero-Based Budgeting | 50/30/20 Rule | Pay-Yourself-First | |

|---|---|---|---|

| How it works | Every dollar assigned to a category before the month starts | 50% needs, 30% wants, 20% savings/debt | Savings automated first; spend the rest freely |

| Effort required | High (15 min/week) | Low | Very low |

| Visibility | Total — you see every dollar’s job | Broad buckets only | Almost none on spending |

| Best for | Debt payoff, tight margins, variable income, chronic overspenders | Stable income with comfortable margin | Disciplined spenders with high income buffer |

| Weakness | Feels tedious; easy to over-engineer | Falls apart when needs exceed 50% | Overspending hides inside “the rest” |

The honest recommendation: if money feels tight, if you’re paying off debt, or if you genuinely don’t know where your money goes, zero-based budgeting is the strongest tool available — precision is exactly what those situations need. If your income comfortably exceeds your lifestyle and your savings rate is already healthy, the 50/30/20 rule or pay-yourself-first will get you 80% of the results for 20% of the effort.

Plenty of people also graduate between methods. They run zero-based budgeting for 12–18 months to kill debt and learn their real spending patterns, then relax into a looser framework once the habits are automatic. That’s not quitting; that’s the method finishing its job.

What to Do When Your Budget Breaks on Day 12

Every first budget breaks mid-month, and how you respond in that moment decides whether you’re still budgeting in March. Here’s the recovery protocol.

Say it’s the 12th. The grocery category has $86 left and three weeks to go, because a birthday dinner and a forgotten pantry restock happened in the same week. The beginner’s instinct is to declare the budget “ruined,” spend freely for the rest of the month, and promise to restart on the 1st. That restart rarely comes.

The zero-based answer is boring and powerful: move money, don’t abandon the plan. Open your budget, find a category that can donate — maybe fun money gives up $40 and the clothing category gives up $60 — and transfer it to groceries. The budget still balances to zero. Nothing is ruined. You made a trade-off consciously instead of pretending it didn’t happen.

This is the single biggest mental shift the method requires: a changed budget is not a failed budget. Corporate finance teams reforecast constantly; nobody at a company says “well, Q2 surprised us, let’s stop doing finance.” Your household deserves the same maturity. The plan is a living document, and editing it mid-month is the system working exactly as designed.

Two guardrails make day-12 surprises rarer over time. First, keep a small “stuff I forgot” category — $50–75 — in every month’s budget. In month one you will forget something (a subscription renewal, a school fee, a parking fine). Second, run a 15-minute weekly check-in, same day every week, where you glance at every category and move money before anything runs dry. Ten minutes on Sunday prevents the Thursday panic.

There’s also a compounding effect worth knowing about. Behavioral researchers call it the planning fallacy — the well-documented human tendency, described by psychologists Daniel Kahneman and Amos Tversky, to underestimate costs and time even when we know we always underestimate. Your first budget will lowball 3–5 categories. Your third budget will lowball one. By month six, your numbers are calibrated against reality, and the budget mostly runs itself. The messy first months aren’t a sign the method doesn’t suit you; they’re the tuition.

Tools That Make Zero-Based Budgeting Easier (Paper, Spreadsheet, or App)

Your tool matters less than your consistency, but the right one for your temperament removes friction, and friction is what kills budgets. You have three real options.

Paper or printable planner. Zero cost, zero learning curve, and the physical act of writing numbers builds awareness faster than any app. The weakness is math: every mid-month money move means recalculating by hand, and errors creep in. Best for people who already keep a paper planner and manage fewer than ~15 categories. A printed monthly budget sheet on the fridge also makes the budget visible to a partner or family, which apps quietly fail at.

Spreadsheet. The sweet spot for most beginners. A simple sheet with columns for planned, spent, and remaining, plus a “left to assign” cell at the top that must read zero, covers everything the method requires. It’s free, it’s yours forever, and it forces you to touch your numbers weekly — which sounds like a downside but is secretly the feature, because awareness is the entire point. Total setup time: about 30 minutes.

Dedicated apps. <a href=”https://www.ynab.com” target=”_blank” rel=”noopener”>YNAB (You Need A Budget)</a> is built entirely around zero-based budgeting and its “give every dollar a job” philosophy; it syncs with bank accounts and handles the math automatically. EveryDollar (from Ramsey Solutions) offers a simpler free tier. Apps cost money — YNAB runs around $109/year — and there’s a real irony in paying a subscription to learn frugality. But for people who abandon manual systems, the automation pays for itself many times over. YNAB’s own user research has long claimed new budgeters save an average of $600 in their first two months, largely by surfacing forgotten subscriptions and unconscious spending.

My honest take after years of watching people try all three: start with a spreadsheet for two months. You’ll learn what categories you actually need and how your spending really behaves. Then, if the manual upkeep is the thing threatening to make you quit — and only then — pay for an app. Buying software before understanding your own patterns is like buying a $200 gym outfit before your first workout.

Common Zero-Based Budgeting Mistakes (That Even Careful People Make)

These aren’t the obvious errors like “don’t overspend.” These are the subtle mistakes that sink people who are genuinely trying.

1. Budgeting the calendar month when your money runs paycheck to paycheck. If you’re paid on the 1st and 15th and your rent clears on the 1st, a monthly view hides a timing crisis: you can have “enough for the month” and still bounce a payment on the 3rd. Fix: until you’ve built a one-month buffer, budget per paycheck. Assign the dollars from this check to the bills due before the next one. Once you’re a full month ahead — spending March’s bills with February’s income — switch to monthly budgeting and the timing stress disappears permanently.

2. Creating 40 micro-categories in a burst of enthusiasm. Separate lines for coffee, snacks, work lunches, weekend food, and “food, other” feels thorough. It’s actually a maintenance tax that guarantees burnout by month two, and it multiplies the number of categories that can “fail” and demoralize you. Fix: start with 12–15 categories maximum. Split a category only after it has confused you for two consecutive months.

3. Treating sinking funds as bonus money when the balance grows. By month eight your car-repair fund holds $400, the car is running fine, and a weekend trip is calling. Raiding it feels harmless — until the timing belt goes in month ten and the “emergency” you specifically pre-funded lands on a credit card anyway. Fix: a sinking fund is spent the moment you assign it. If your priorities genuinely changed, formally rename and repurpose the category during your monthly planning session — decide it on paper, never at the checkout.

4. Budgeting your aspirational self instead of your actual self. Writing $200 for groceries because that’s what a disciplined person would spend — while your last three statements say $520 — doesn’t make you disciplined. It makes your budget fictional, and you can’t steer with fiction. Fix: month one uses last month’s real numbers, however ugly. Reduce any category by no more than 10–15% per month. Slow cuts hold; dramatic cuts snap back.

5. Leaving your partner out of the plan. One person builds a beautiful budget, the other keeps spending like it doesn’t exist, and by month three the budgeter is resentful and the budget is dead. Money conflict is consistently ranked among the top sources of relationship stress in family-finance research. Fix: build the budget together in a 30-minute monthly session, and give each person their own no-questions-asked fun money category. Autonomy inside the plan is what makes the plan survivable for two people.

FAQ

What does zero-based budgeting mean in simple terms? It means you plan a job for every dollar of your income before the month starts, until income minus planned spending equals exactly zero. Rent, groceries, savings, debt, and fun money each get a set amount. Nothing is left floating and unassigned. Money put into savings counts as assigned — zero refers to your plan, not your bank balance.

Is zero-based budgeting good for beginners? Yes, especially if money feels tight or you honestly don’t know where your paycheck goes. It’s more hands-on than other methods — expect about an hour of setup and 15 minutes a week — but that visibility is exactly what beginners are missing. Start with a simple spreadsheet and 12–15 categories, and expect the first two months to be calibration, not perfection.

What’s the difference between zero-based budgeting and the 50/30/20 rule? The 50/30/20 rule sorts income into three broad buckets: 50% needs, 30% wants, 20% savings and debt. Zero-based budgeting assigns every dollar to specific named categories instead. The 50/30/20 rule is faster but vaguer; zero-based gives total control but takes more effort. Tight margins or debt payoff favor zero-based; comfortable margins do fine with 50/30/20.

Does zero-based budgeting mean my bank account should be at zero? No — this is the most common misunderstanding. The “zero” means zero unassigned dollars in your plan, not zero money in your account. Your account should actually hold a growing buffer, because dollars assigned to savings, sinking funds, and next month’s bills sit in the bank doing their assigned jobs. A healthy zero-based budgeter’s balance usually rises over time.

How do I do zero-based budgeting with irregular income? Budget using the lowest monthly income from your last six months as your baseline, and fund essentials first: housing, food, utilities, transport. When a better-than-baseline month arrives, assign the extra dollars in priority order — buffer first, then debt or savings. Never build the plan around your best month. Freelancers should also prioritize building one full month of expenses as a buffer.

Closing

The core of zero-based budgeting is one sentence: decide what every dollar will do before the month begins, so the decision never has to happen when you’re tired, tempted, or standing at a checkout. Your budget will bend mid-month — that’s the system working, not breaking — and each month’s plan gets sharper than the last. Open your banking app tonight, pull last month’s real numbers, and give next month’s first dollar its job before the 1st arrives.